.

.

.

.

.

.

India's trade is about $822 billion for 2014, and about 15% of the $5.5 trillion PPP GDP.

India's growth has not come from EXPORTS, but from domestic investment and consumption.

So a slump in Exports from the $336 billion figure of 2014 is nothing to worry about in any real sense.

AND again NO......there is no correlation between India's domestic investment and consumption led growth, and general global decline in demand due to the slowing of the Chinese economy, Europe and an USA economic collapse.

India needs to re-orientate its focus on trade with STILL buoyant economies like Japan, South Korea.....yes China, Russia, Persia, SAARC neighbors, ASEAN ........and so forth in anticipation of economic slump in the EU and North America.

Readjustment of trading priorities to meet the very reasonable figure of $900 billion exports for 2019. The Indian government may wish to play a significant role in this direction.

AND finally I repeat again, the Soviet model under Comrade Stalin between 1928--1941...where his command economy, under detailed planning achieved on average 20% GDP growth rates year in year out. Obviously the totalitarian government exacted a heavy sacrifice from the population (butter and jam tomorrow), which would be politically unacceptable in Democratic India. BUT that is not the point of the argument. The point is that despite sanctions by the Western powers, and the Great Depression of the late 1920's and early 1930's.....the Soviet Union still achieved through heavy INVESTMENT in INDUSTRY and INFRASTRUCTURE remarkable economic growth.......and the secret source of China's economic miracle since 1980, with the aid of foreign capital investment, and Capitalist legal instruments in specialized trading Zones, through the far sighted leadership of Deng Xiaoping.

__________________________________________________

Export slump cast shadow on growth prospects

Reuters and Times of India.

India's exports slumped

for the fifth straight month in April from a year earlier, dragged down

by fall in global demand that has cast a shadow over Prime Minister Narendra Modi's goal of achieving over 8 per cent growth in 2015/16 fiscal year.

The ongoing weakness in merchandise exports, which account for about 16

per cent of India's roughly $2 trillion economy, will weigh on January

to March economic growth numbers due to be released on May 29.

Modi sees manufacturing and export-led growth as the best way to create

jobs for the millions of young people who helped him gain power last

year.

Modi sees manufacturing and export-led growth as the best way to create

jobs for the millions of young people who helped him gain power last

year.

He aims to almost double goods and services exports to $900 billion in the next four years.

But merchandise exports contracted 14 per cent in April. The trade

deficit narrowed to $10.99 billion as oil imports declined by more than

42 per cent from a year earlier, data released by Ministry of Commerce

and Industry showed on Friday.

Exporters said falling

global commodity and crude oil prices had so far partly offset their

lower overseas sales, but they fear more gloom - as demand is falling

further, particularly in oil exporting and Latin American countries.

"There is a fall in order booking for coming months, particularly from

buyers in the Middle East, Africa and Latin American countries," said

Ajay Sahai, a senior executive at the Federation of Indian Export

Organisations.

He warned that exporters could be forced to lay off workers if sales orders continued to decline over the next 4-5 months.

Some relief could come from the Reserve Bank of India, which has cut

policy rates twice this year to 7.5 per cent because of slower consumer

inflation, and is expected to make borrowing cheaper again when it meets

for a policy review on June 2.

To counter slack global demand, Modi has vowed to modernise overloaded

roads, ports and railways in a bid to make India's exports more

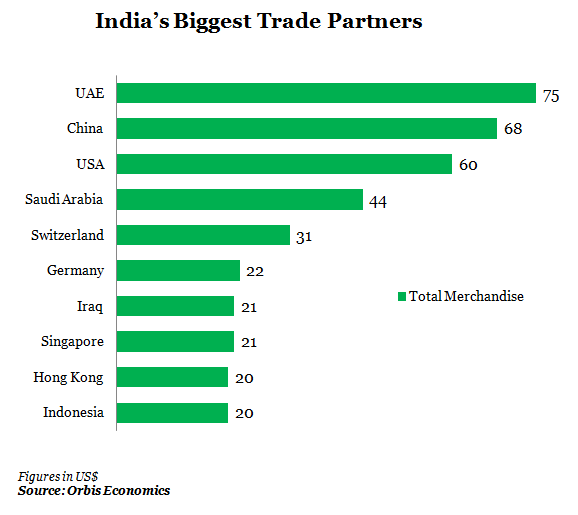

competitive. This week, he is visiting top trading partner China, hoping

to invigorate exports.

India's economy expanded 7.5 per cent

year-on-year during the three months ending in December, higher than

China's 7.3 per cent growth recorded in that quarter.